[DIGITAL Business Africa] – As the 14th Ministerial Conference of the World Trade Organisation (WTO), scheduled for 26 to 29 March 2026 in Yaoundé, approaches, Cameroon cannot limit itself to the role of a purely ceremonial host.

Hosting MC14 imposes a particular political responsibility on Cameroon: to actively contribute to the search for credible compromises on the most sensitive issues in multilateral trade.

The current negotiating context, marked by sharp divergences on electronic commerce and on the moratorium on customs duties applicable to electronic transmissions, calls for a structured, credible and, above all, operational positioning. This responsibility requires Cameroon, through its relevant administrations, to take concrete steps to advance its proposals at the earliest opportunity at the next meeting of the WTO Work Programme on Electronic Commerce, scheduled for 2 March 2026 in Geneva.

Substantively, the WTO debate is now crystallising around two major fault lines. The first concerns the orientation of the Work Programme on Electronic Commerce, which is viewed as insufficiently operational in addressing development challenges. The second concerns the moratorium in place since 1998, regularly extended but increasingly contested due to its fiscal implications.

A debate now framed by a clear deadline set by ministers at MC13

This debate is also taking place within a political and legal framework that WTO ministers clearly defined at the 13th Ministerial Conference (MC13), held in Abu Dhabi from 26 February to 2 March 2024. In their Ministerial Decision on the Work Programme on Electronic Commerce, adopted on 2 March 2024, ministers agreed to continue reinvigorating the Work Programme, with particular emphasis on its development dimension, taking into account the economic, financial and development needs of developing and least developed countries.

Most importantly, ministers explicitly decided to maintain the practice of not imposing customs duties on electronic transmissions only until the 14th Ministerial Conference or until 31 March 2026, whichever is earlier, stating unambiguously that the moratorium and the Work Programme will expire on that date.

This decision marks a major turning point. For the first time since 1998, the moratorium extension is no longer automatic or open-ended, but is explicitly time-bound. Ministers also requested that discussions be deepened on the scope, definition and impact of the moratorium, drawing on empirical evidence, notably in relation to development, digital industrialisation, and the ability of developing and least-developed countries to “level the playing field” in the digital economy.

It is therefore within this specific context—of a programmed end-date for both the moratorium and the Work Programme, as decided at MC13—that the discussions held in Geneva in January 2026, the decisive meeting of 2 March 2026, and MC14 in Yaoundé fully take on their meaning. The challenge is no longer merely to extend the status quo, but to define the future of the multilateral framework for electronic commerce on foundations that are more balanced, better documented, and more attentive to fiscal and development realities.

Understand the moratorium

Opposing camps on the moratorium

On the moratorium, two camps are openly opposed. On one side, several Members support the continuation, and even the permanence, of the moratorium. The United States, the European Union, Japan, Canada, Australia and Singapore are among the most consistent supporters of this position.

Other Members, including China, also support renewing the moratorium, while at times expressing nuances aligned with their development priorities. These countries emphasise the stability of the digital trade framework, predictability for businesses, and the promotion of innovation.

On the other side, a group of developing countries is increasingly opposed to an automatic renewal of the moratorium. India, South Africa and Indonesia are the most visible in this camp. They explicitly cite concerns about potential losses of public revenue, the shrinking of fiscal and industrial policy space, and the lack of clarity regarding the definition of “electronic transmissions” in a context of rapidly accelerating digitalisation of trade.

Since 1998, the moratorium has helped create an environment of stability and predictability for the growth of global e-commerce. For many companies—especially in digitally advanced economies such as the United States, the European Union, Japan, Canada, Australia and Singapore—the absence of customs duties on electronic transmissions has become a structuring element of digital business models and a key confidence factor for investment and innovation.

However, as goods that were once traded physically are increasingly delivered digitally—such as software, cultural content, and dematerialised services—the fiscal implications of the moratorium are becoming more visible for developing and least developed countries. In these economies, customs duties remain an important source of public revenue, and the progressive digitalisation of trade raises legitimate questions about potential revenue losses and the narrowing of fiscal policy space.

In this polarised landscape, Cameroon has an opportunity to play a facilitating role by advancing three complementary proposals, respectively addressing the discussion framework, the taxation of digital trade, and the legal governance of the digital economy.

The first proposal: strengthening the discussion framework through a clearer development track

The first proposal concerns reinvigorating the WTO’s framework for discussions on electronic commerce. It could be formulated as follows:

“MINISTERS AGREE TO FURTHER STRENGTHEN THE WORK PROGRAMME ON ELECTRONIC COMMERCE, IN PARTICULAR BY MORE CLEARLY STRUCTURING ITS DEVELOPMENT DIMENSION, IN ORDER TO SUPPORT THE PROGRESSIVE PARTICIPATION OF DEVELOPING AND LEAST-DEVELOPED COUNTRIES IN GLOBAL ELECTRONIC COMMERCE.”

This proposal fully aligns with the continuity of decisions adopted at the 12th and 13th Ministerial Conferences and with the positions defended by the African, Caribbean and Pacific (ACP) Group. It does not challenge the WTO acquisaddres but rather seeks to correct a persistent structural weakness: the absence of a clear operational framework to translate development principles into concrete action in the field of electronic commerce.

Indeed, since its adoption in 1998, the Work Programme on Electronic Commerce has recognised the relevance of development issues in digital trade discussions. Yet this development dimension has remained implicit and cross-cutting, without clear institutional structuring or a dedicated track.

While the Programme has provided a useful forum for dialogue, it has not, to date, ensured systematic and continuous consideration of the specific needs of developing and least developed countries as electronic commerce takes up an increasing share of global trade.

Ministerial decisions adopted at the 12th and 13th Ministerial Conferences marked important progress by calling for the reinvigoration of the Work Programme, with a particular emphasis on its development dimension. These decisions sent a strong political signal, recognising the growing development implications of electronic commerce. However, they did not establish a dedicated mechanism, define clear operational mandates, or specify expected outputs, leaving the development focus largely declaratory—something Cameroon’s proposal could help address.

Unlike the 2024 Ministerial Decision, which recognises the centrality of development without altering the institutional architecture, Cameroon’s proposal seeks to transform that political orientation into a structured and readable framework by explicitly introducing the principle of the progressive participation of developing and least-developed countries in global electronic commerce. In short, MC13 said “development matters”, while Cameroon’s proposed MC14 says “here is how to organise it”.

WTO E-Commerce Discussions: Existing Framework vs. Cameroon’s Added Value

| KEY ELEMENTS | WHAT ALREADY EXISTS AT THE WTO | THE “ADDED VALUE” OF CAMEROON’S SUGGESTED PROPOSAL |

| Status of development within the Work Programme | Development recognised as a cross-cutting issue since 1998, without a dedicated structure | Creation of a clearly identified, structured development track |

| Nature of commitments | Broad political orientations, without precise operational mandates | Clarification of a functional framework to translate orientations into action |

| MC12 and MC13 decisions | Call to revitalise the Programme with a focus on development | Concrete deepening through a more readable internal organisation |

| ACP proposals | Strong emphasis on development, cooperation and revitalisation | Shift from declaratory logic to institutional structuring |

| Programme governance | Discussions dispersed across themes and sessions | Improved readability through a dedicated development pillar |

| Participation of developing countries and LDCs | Implicitly recognised through special and differential treatment | Explicit recognition of progressive participation in e-commerce |

| Flexibility and policy space | Present in the WTO system but weakly articulated for e-commerce | Clear integration of flexibility into digital discussions |

| Digital capacities | Technical assistance mentioned in general terms | Stronger link between e-commerce discussions, digital capacities and targeted support |

| Link with Annex 4 (LDCs) | Fragmented approach, without explicit articulation | Coherence between accession, development and e-commerce |

| Plurilateral digital agreements | Voluntary participation, but implicit political pressure | Reaffirmation of freedom of progressive, non-mandatory participation |

| Strategic vision | Issue-by-issue management | Structured vision of inclusive, development-oriented e-commerce |

| Political positioning | No clearly identified geographic leadership | Positioning Cameroon as a facilitator and North–South bridge as MC14 host |

This proposal does not challenge the existing WTO framework on electronic commerce; it strengthens its coherence and effectiveness by translating broad political orientations into a structured, readable and development-oriented mechanism.

The second proposal: the moratorium and the centrality of digital taxation

Cameroon’s second proposal directly addresses the moratorium on electronic transmissions and places digital taxation at the centre of the debate. It could be framed as follows:

“MINISTERS AGREE TO EXTEND THE MORATORIUM ON CUSTOMS DUTIES APPLICABLE TO ELECTRONIC TRANSMISSIONS UNTIL THE NEXT MINISTERIAL CONFERENCE, WHILE SUBSTANTIALLY STRENGTHENING ANALYTICAL WORK ON ITS FISCAL, ECONOMIC AND DEVELOPMENT IMPACTS FOR DEVELOPING AND LEAST-DEVELOPED COUNTRIES, IN ORDER TO INFORM ANY FUTURE DECISION.”

This approach enables Cameroon to avoid a binary position. It recognises the usefulness of the moratorium for short-term stability in digital trade, while fully legitimising the fiscal concerns expressed by several countries of the Global South. Above all, it opens the way to precise, sector-specific, empirically grounded studies, allowing developing countries to realistically assess the effects of electronic commerce on their public revenues.

Digital taxation cannot remain a blind spot in WTO discussions. For many African countries, customs duties remain a critical source of public revenue. The progressive dematerialisation of trade therefore poses a major fiscal sustainability challenge. Without rigorous analysis of potential revenue losses—and of the capacity to compensate through other fiscal instruments—the moratorium debate will remain fragile and politically divisive.

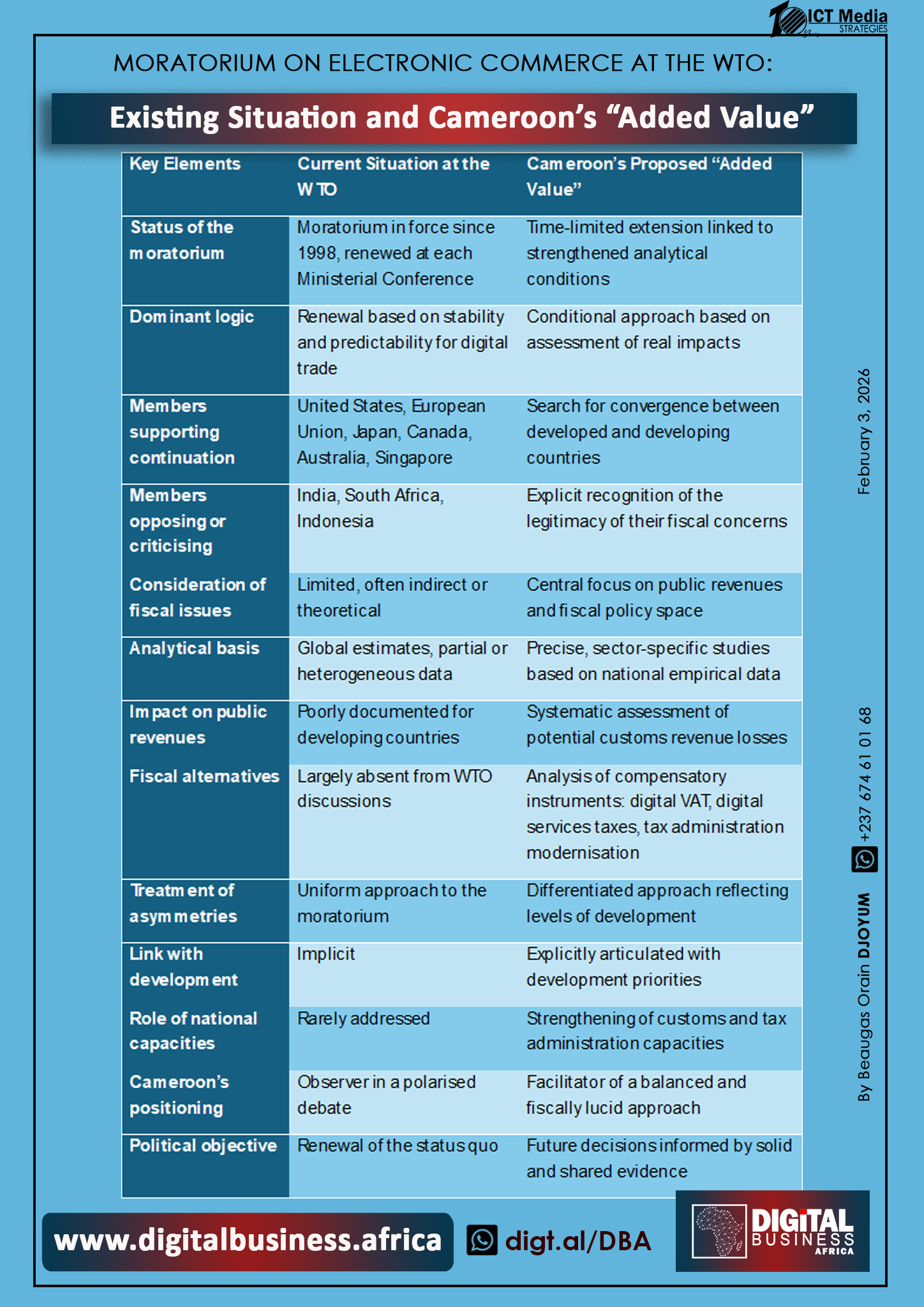

Moratorium on e-commerce at the WTO: what exists and Cameroon’s “added value”

| KEY ELEMENTS | CURRENT SITUATION AT THE WTO | THE “ADDED VALUE” CAMEROON COULD PROPOSE |

| Status of the moratorium | In place since 1998, renewed at each Ministerial Conference | Time-limited extension linked to strengthened analytical conditions |

| Dominant logic | Renewal based on digital trade stability | Conditional approach based on real-impact assessment |

| Countries supporting extension | United States, EU, Japan, Canada, Australia, Singapore | Search for convergence between developed and developing countries |

| Countries opposing/criticising | India, South Africa, Indonesia | Explicit recognition of the legitimacy of fiscal concerns |

| Consideration of taxation | Limited, often indirect or theoretical | Making public revenues and fiscal policy space central to the debate |

| Analytical base | Global estimates, partial or heterogeneous data | Precise, sectoral studies grounded in national empirical data |

| Impact on public revenues | Poorly documented for developing countries | Systematic assessment of potential customs revenue losses |

| Fiscal alternatives | Rarely integrated in WTO discussions | Analysis of compensatory tools: digital VAT, taxation of digital services, tax modernisation |

| Treatment of asymmetries | Uniform approach | Differentiated approach reflecting levels of development |

| Link to development | Implicit | Explicitly articulated with development priorities |

| Role of national capacities | Weakly addressed | Strengthening capacities of tax and customs administrations |

| Cameroon’s positioning | Observer in a polarised debate | Facilitator of a balanced and fiscally lucid approach |

| Political outcome | Status quo renewal | Future decisions informed by solid, shared evidence |

Cameroon’s proposed approach does not challenge the moratorium on electronic commerce; it seeks to move the debate beyond an ideological standoff by placing digital taxation, public revenues and data-driven analysis at the centre of multilateral decision-making.

The case of the Plurilateral Agreement on Electronic Commerce: openness without haste

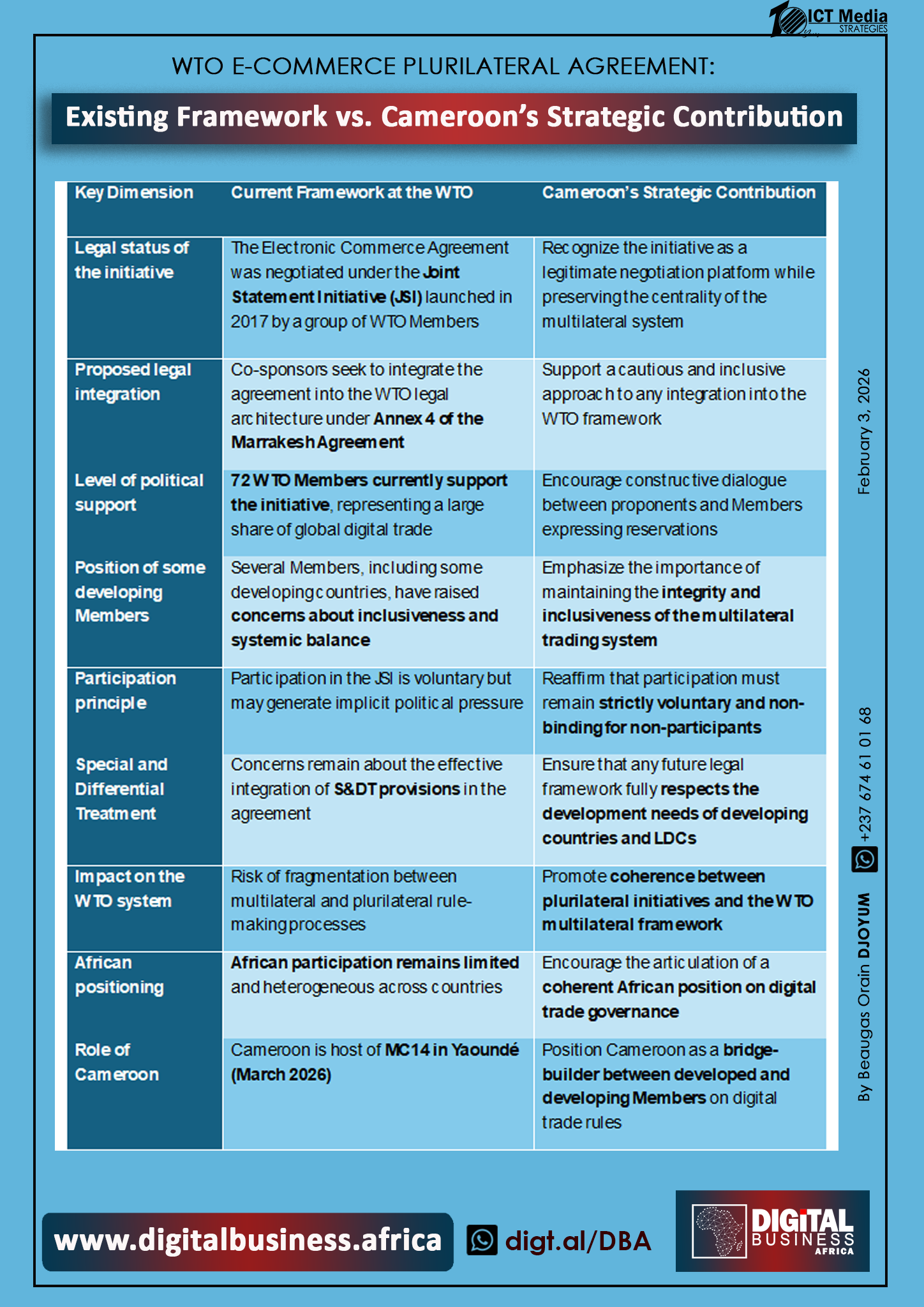

Finally, the WTO e-commerce debate cannot ignore the issue of the plurilateral Agreement on Electronic Commerce, whose request for incorporation into the WTO legal architecture under Annex 4 of the Marrakesh Agreement did not secure consensus at the General Council in December 2025. The request for Annex 4 incorporation, available since December 2024, was formally brought before the General Council in late 2025.

While 72 co-sponsors support this initiative and formally requested in December 2025 that the WTO incorporate it into Annex 4 of the WTO Agreements, several WTO Members—including India, South Africa and Indonesia, among other developing countries—expressed reservations, recalling the need to preserve inclusiveness and balance in the multilateral system. Among the 72 co-sponsors of this plurilateral agreement are six African countries: Benin, Burkina Faso, Cabo Verde, The Gambia, Kenya and Mauritius.

At the WTO, discussions on electronic commerce take place in two distinct but complementary tracks. On the one hand, the Work Programme on Electronic Commerce was established in 1998 to examine, in an exploratory manner, the relationship between existing WTO agreements and electronic commerce, without negotiating new formal rules.

On the other hand, a group of Members launched in 2017 the Joint Statement Initiative on Electronic Commerce (JSI), a plurilateral negotiating process open to all WTO Members, aimed at developing new and more binding rules on electronic commerce. Co-led by Australia, Japan, and Singapore, this initiative reflects a voluntary approach by Members who wish to move faster in digital disciplines.

After more than five years of negotiations under the JSI, a stabilised text of the Agreement on Electronic Commerce was published on 26 July 2024, marking a major milestone in the development of digital trade rules at the WTO.

According to the WTO, the Members participating in the JSI discussions represent more than 90% of world trade, although acceptance of the stabilised text is not yet unanimous among them.

What the plurilateral Agreement on Electronic Commerce provides in practice (Article 11)

The plurilateral Agreement on Electronic Commerce, resulting from the WTO’s JSI and finalised in July 2024, contains a specific provision on customs duties on electronic transmissions. Article 11 establishes three key principles:

-

Prohibition of customs duties on electronic transmissions (Article 11.3)

No Party shall impose customs duties on electronic transmissions between a person of one Party and a person of another Party.

This makes the moratorium principle legally binding among the Parties to the Agreement.

2. Scope for internal taxation (VAT, digital taxes, etc.) (Article 11.4)

For greater certainty, paragraph 3 does not preclude a Party from imposing internal taxes, fees, or other charges on electronic transmissions in a manner not inconsistent with the WTO AgreemenT.

The Agreement explicitly recognises internal fiscal sovereignty: VAT on digital services, platform taxes and other internal charges consistent with WTO rules are permitted, provided they do not amount to discriminatory treatment inconsistent with WTO agreements.

3. Periodic review clause (but no automatic reversal) (Article 11.5)

Taking into account the evolving nature of electronic commerce and digital technology, the Parties shall review this Article in the fifth year after the date of entry into force of this Agreement, and periodically thereafter, with a view to assessing the impacts of this Article and whether any amendments are appropriate.

There is a review clause after five years (supported by some developing countries during the negotiations). However, this clause is internal to the plurilateral Agreement, does not automatically allow suspension of the prohibition on customs duties, and does not condition the prohibition on fiscal studies or revenue impacts.

In this context, as a third proposal, Cameroon could adopt a prudent posture of openness. It may recognise the legitimacy of the plurilateral initiative, while emphasising that any legal incorporation must remain strictly voluntary, respect special and differential treatment, and create no direct or indirect pressure on developing and least-developed countries.

For Cameroon, the priority may remain the consolidation of the existing multilateral framework, notably through an effective and structured strengthening of the Work Programme on Electronic Commerce, before any legal advancement on plurilateral agreements.

Cameroon’s action

It is therefore crucial that Cameroon, through coordinated action by the Ministry of Trade, the Ministry of External Relations, Cameroon’s Permanent Mission to the WTO in Geneva, and the relevant technical administrations, take all necessary steps to bring these proposals to the next meeting of the WTO Work Programme on Electronic Commerce on 2 March 2026 in Geneva.

This is, more specifically, a multilateral working session preparing for the 14th WTO Ministerial Conference (MC14), which will take place from 26 to 29 March 2026 in Yaoundé, Cameroon.

This meeting follows directly from the exchanges on 28 January 2026, during which WTO Members examined prospects for reaching an outcome on electronic commerce at MC14, particularly on revitalising the Work Programme; the moratorium on customs duties on electronic transmissions; and potential elements for a ministerial decision in Yaoundé.

This is where Cameroon’s credibility will be tested—as a convergence actor and as host of a Ministerial Conference expected to deliver substantive outcomes.

With only a few weeks remaining before MC14 in Yaoundé, Cameroon has an important diplomatic window to contribute to a more mature, better informed and fairer debate on the future of electronic commerce.

By combining a development-centred reinvigoration of the Work Programme with a fiscally sound approach to the moratorium, Cameroon can help bring today’s antagonistic positions closer together and anchor multilateral digital trade on a truly inclusive trajectory.

Beyond MC14, this approach could also serve as the basis for a structured African contribution to the global debate on digital trade governance—reconciling openness, fairness and fiscal sustainability. The call for empirical analysis also aligns with ongoing discussions in other international fora on the taxation of the digital economy and could help Africa carry greater weight in shaping the rules of global digital trade.

By Beaugas-Orain DJOYUM

Publisher of Digital Business Africa and CEO of ICT Media STRATEGIES

{kind=link}